Even though we are still over a week away from the half-way mark, this year has been a very eventful one for the financial markets.

This eventfulness can be attributed to President Trump in a significant way.

His administration has also been involved in the tragedy in the Near East.

It’s been a bad start. The team of Trump is now involved in talks with Tehran. Most of the world hopes for an improved outcome and a halt to Iran’s nuclear plans. Trump is also busy at home.

The House of Representatives barely passed his tax bill.

Many are hopeful that the Senate will approve the bill, which could give the US economy an economic boost through (diluted) spending and tax cuts. This would be despite the fact that the debt is increasing significantly.

The market has been primarily focused on President Trump’s proposed tariffs against US imports.

Investors have been spooked by the uncertainty created by tariffs and their erratic distribution.

Tariffs are the best excuse for the US Federal Reserve to delay further rate reductions (having already slashed 100 basis points from the Fed Funds Rate over the final four months of 2020) and provide cover to Moody’s in order to reduce the US’s rating.

Moody’s is looking rather vulnerable since Fitch cut US credit in August 2023. They are now joining S&P, who beat both of them and created a much bigger commotion when they downgraded US credits in 2011.

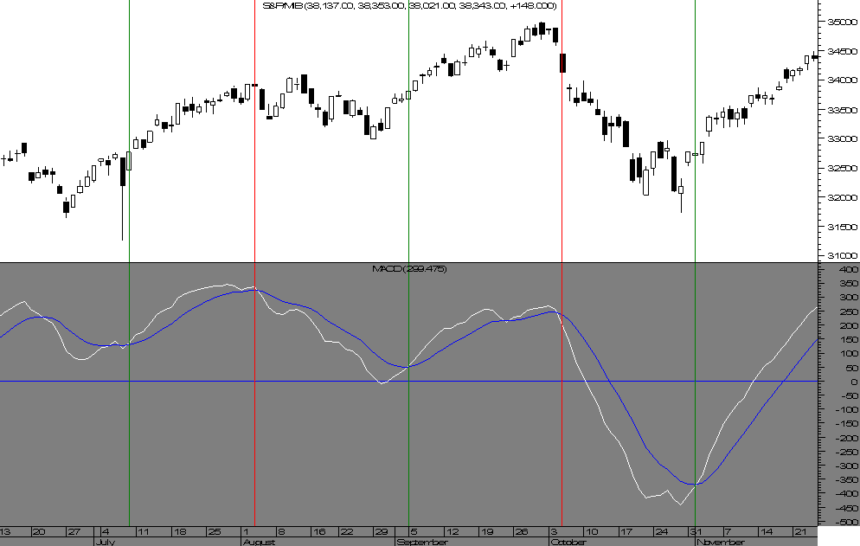

Looks like several markets have reached an inflexion, consolidating recent movements while giving little clues as to where they might go next. The US stock indexes seem to want the rally to continue.

They have come far from their lows in April, after their initial negative reaction to Trump’s first tariff announcement.

According to the MACDs of their respective US majors, as the end of May approaches, they continue to appear overbought.

This could indicate that they will sell from now on. Their MACDs may also be corrected by a prolonged period of consolidation.

Mid-April, when gold reached a record high of $3500, it was a signifi cant overbought.

The price of silver has since pulled back and the MACD daily has fallen to neutral levels. Since mid-April, silver has been in a narrow range of $1.50.

The support has been around $32 an ounce while the resistance has limited the upward movement to $33.50.

Silver’s MACD daily has been tracking sideways again, around neutral levels. After finally crossing above $2,000 at the beginning of 2024, gold has seen a number of new record highs.

Silver is still far from its April 2011 high of $50.

As we move into summer and beyond, both have big potential to grow. It’s just a matter of deciding which way to go.

Since March 2022, when Russia invaded Ukraine, crude oil has seen a steep decline. The daily MACD is also back to neutral. It appears that the oil market has been trapped within a narrow range. Every rally has been met with resistance. How much longer can this last?

Hyman Minsky said that “stability breeds instability”. Sometimes markets require a catalyst in order to make a major move.

Tarife could trigger the event. It could also be one of Donald Rumsfeld’s “unknown unknowns”. Don’t be shocked if volatility increases in the future.

David Morrison, Senior Market Analyst for Trade Nation. His views are his. )

The post on Consolidation of the Markets may change as new information is released.

This site is for entertainment only. Click here to read more